Understanding your salary slip helps you get a clear picture of where your money goes and can help you catch errors, make the most of benefits, and negotiate smarter. It’s also crucial for optimising tax savings and future planning.

Before we get into how you can maximise your take-home pay.

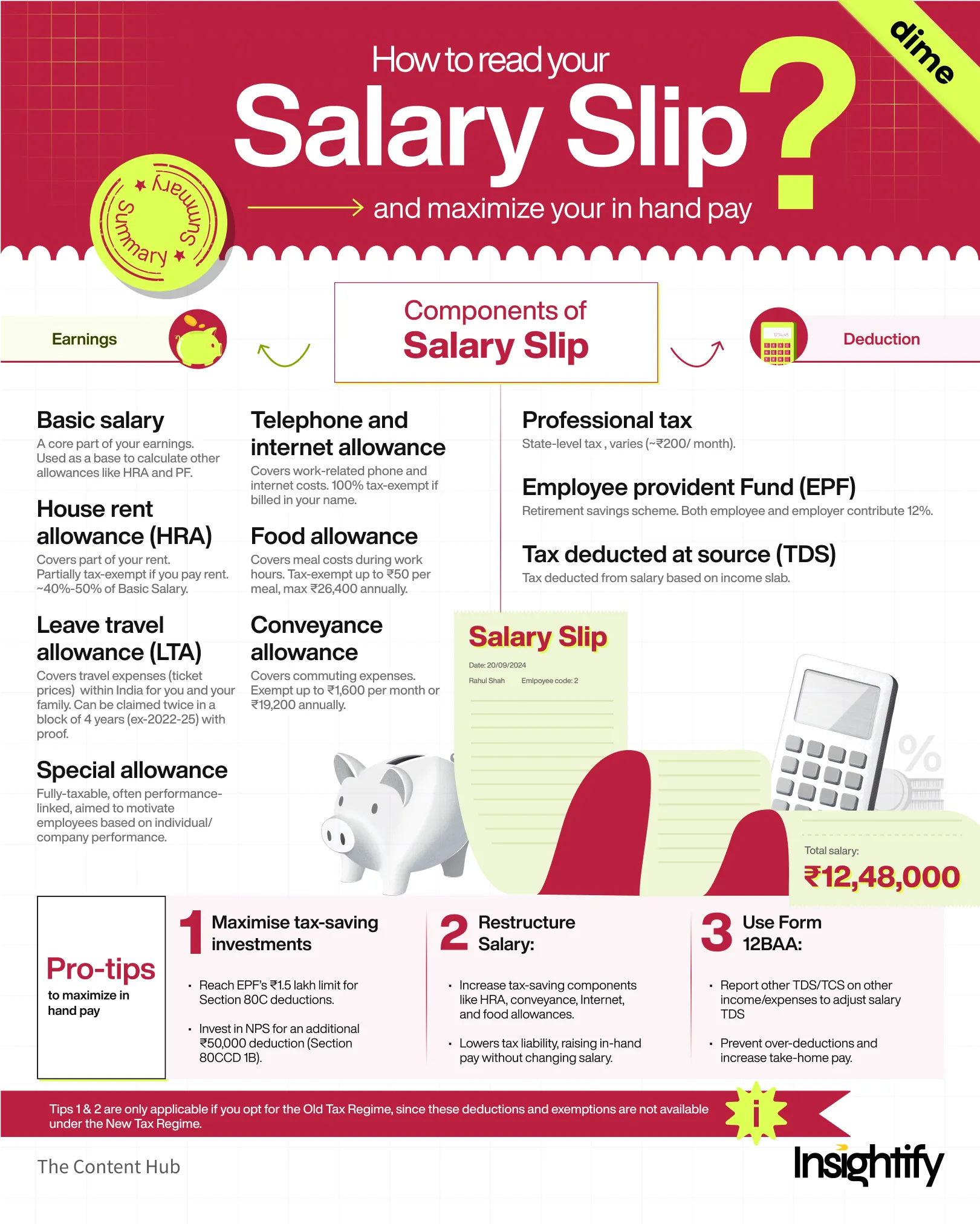

Let’s break down the components of your salary slip

Earnings

~add{num,1}

Basic Salary

This is the core part of your earnings apart from benefits and privileges and is also used as a base to calculate other allowances like HRA and PF.

It typically forms around 40%-60% of your total pay during the early stages of your career and decreases in proportion as you move up the corporate ladder.

~add{num,2}

House Rent Allowance (HRA)

HRA helps cover your rent expenses and is partially tax-exempt if you pay rent. It is credited to your account monthly and usually ranges between 40%-50% of your basic salary.

~add{num,3}

Flexible Benefit Plan (FBP)

A Flexible Benefit Plan (FBP) allows you to customise parts of your salary package to meet personal expenses and reduce tax. Through FBP, you can structure your CTC with tax-exempt benefits, reducing your taxable income and increasing in-hand pay.

If your company doesn’t offer FBP you might be getting these allowances separately.

~add{18,blog_highlight-block}

a) Leave Travel Allowance (LTA)

LTA allows you to claim travel expenses (just the ticket prices) for you and your family within India. You can get a tax exemption twice in a block of four years, such as between 2022-2025, provided you submit proof of travel.

b) Telephone and Internet Allowance

This allowance covers work-related phone and internet expenses. Employees can claim 100% tax exemption with proper billing. Many companies have a cap for this reimbursement, which can be negotiated.

c) Conveyance Benefits

Fuel allowance: Employees can claim fuel expenses by submitting bills to employers. This allowance is tax-free up to ₹2,400/month. If no bills are submitted, the allowance is fully taxable.

Employee’s personal car: Companies may provide vehicles for official use, with tax exemption on related fuel bills when used exclusively for business purposes. For mixed use, the employer covers a part, and the rest is taxable for the employee.

Company car: Select employees may receive a company car. To claim tax-free fuel expenses, proof of business use is required.

Driver allowance: Typically offered to executive roles, covering driver costs up to ₹900/month, tax-free if receipts are submitted.

d) Food Allowance

Employers often provide meal vouchers or prepaid cards like Sodexo. You can claim up to ₹50 per meal as a tax exemption, with a maximum annual tax-free benefit of ₹26,400.

e) Conveyance Allowance

Conveyance allowance covers your commute expenses. It is tax-exempt up to ₹1,600 per month or ₹19,200 annually.

f) Professional Development

Covers expenses like training, seminars, and skill development courses. This allowance is fully tax-exempt if receipts are provided, fostering employee growth without tax impact.

g) Books and Periodicals

Allows employees to claim reimbursements for books and journals related to professional growth. Tax exemption applies with valid receipts, with limits set by the employer.

h) Gift Card

Employers may provide gift cards up to ₹4,999 annually, tax-free. This is a popular FBP option, allowing employees to enjoy non-cash rewards without tax impact.

i) Gadgets & Equipment

Includes devices for professional use, like laptops or phones, with tax-free benefits up to ₹60,000 annually upon valid expense claims. This allowance supports productivity without additional tax.

Deductions

~add{num,1}

Professional Tax

Professional tax is levied by state governments on income earned through employment or profession. It’s typically around ₹200 per month but varies across states. It’s deducted to fund state welfare programs and is capped at ₹2,500 annually.

~add{num,2}

Employee Provident Fund (EPF)

EPF is a mandatory deduction on your salary slip, where 12% of your basic salary is contributed towards your retirement savings. This is reflected each month and is matched by an equal contribution from your employer.

~add{num,3}

Tax Deducted at Source (TDS)

TDS is deducted from your salary based on your tax slab. It helps you manage your tax liability by spreading payments throughout the year, preventing the burden of a large tax payment at the end of the year. The deducted amount is reflected in your Form 16, which can be used to file your income tax return.

That’s the complete break-down of a salary slip!

Here are a few pro tips to maximise your in-hand pay!

~add{num,1}

Utilise tax-saving investments

If your EPF contribution doesn’t hit the ₹1.5 lakh limit under Section 80C, you can top it up with investments in PPF or ELSS to fully utilise the deduction. Even if your PPF reaches the cap, you can invest in the NPS and claim an additional ₹50,000 deduction under Section 80CCD (1B). Remember, these deductions are only available under the Old Tax Regime.

~add{num,2}

Use form 12BAA to lower TDS

Form 12BAA lets you inform your employer about any TDS or TCS already paid on other income, like interest, dividends, or large expenses. This helps your employer adjust your salary TDS based on these additional taxes, preventing over-deductions and increasing your monthly take-home pay while avoiding the hassle of refunds later.

~add{num,3}

Restructure your salary

Let’s see how Rohan leverages flexible benefits to restructure his annual salary and maximise tax-saving allowances on his actual expenses to increase his in-hand pay (along with the following Tip 1).

By optimising his Flexible Benefits Plan, Rohan maintains his gross income at ₹24.4 lakhs but reduces his Tax liability by ₹53,664!

This restructuring doesn’t change his total income but maximises his in-hand pay by reducing his Tax Liability.

Note: Most exemptions and deductions aren’t available in the New Tax Regime, so salary restructuring can’t increase in-hand pay if you choose the New Tax Regime.

Wondering which regime to choose? Here’s your solution!

Hope this helps! If you are wondering how exemptions and deductions can help you save more on taxes, go, check this out!

~add{3,blog_highlight-block}

Summary

To make your life easier, we have summarised the above Read here. Hope you enjoyed it!

Be the CEO of your Finances

Get practical and actionable money insights delivered straight to your inbox.