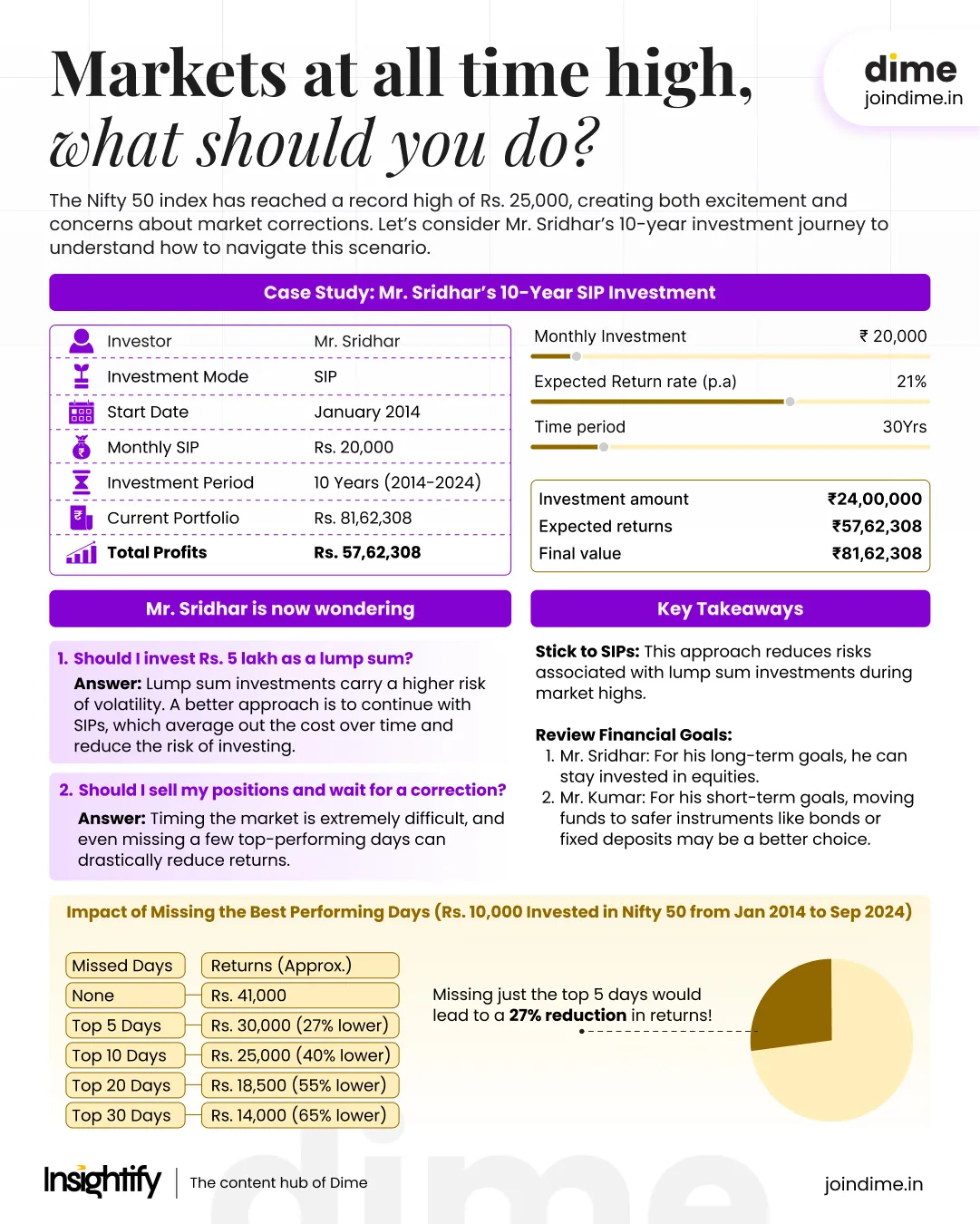

The Nifty 50 index has reached a record high of 25,000, with many small-cap and mid-cap stocks also touching their peak levels.

For retail investors, this is both exciting and daunting, as market highs can create a fear of missing out (FOMO), while also raising concerns about potential corrections.

To better understand how to navigate such scenarios, let’s look at the real-life example of Mr. Sridhar.

Case study: Mr. Sridhar’s 10-year investment journey

- Investor: Mr. Sridhar, Software Engineer

- Investment Mode: Systematic Investment Plan (SIP)

- Start Date: January 2014

- Monthly SIP Amount: Rs. 20,000

- Investment Period: 10 years (Jan 2014 – Sep 2024)

- Current Portfolio Value: ~Rs. 81,62,308

- Profits: ~Rs. 57,62,308

Mr. Sridhar is extremely happy with his returns

But as markets rise, he is faced with two choices

Should I invest Rs. 5 lakh as a lump sum now to benefit from rising markets?

Should I sell my positions and wait for a market correction to reinvest?

Answering Mr. Sridhar’s questions

~add{num,1}

Should I invest Rs. 5 lakh as a lump sum immediately?

It’s tempting to invest a large amount when markets are rallying, but this exposes you to short-term volatility. If the market corrects right after your investment, your lump sum could lose value quickly.

~add{2,blog_highlight-block}

Better approach, Continue SIPs: SIPs help average the cost over time and reduce the risk of investing at market highs.

Mr. Sridhar has seen success with SIPs over the last 10 years, so continuing this strategy allows him to avoid the need to time the market while still benefiting from long-term growth.

~add{num,2}

Should I sell my positions and wait for the market to correct?

Timing the market is very difficult, even for experts.

Trying to sell at the market’s peak and buy back during a dip is known as timing the market, and it’s extremely hard to get right. Even missing a few of the best-performing days can drastically reduce your returns.

Why staying invested is often better?

If you had invested Rs. 10,000 in Nifty 50 in January 2014, it would have grown to approximately Rs. 41,000 by September 2024. However, if you missed the top 5 performing days, the same investment would only be worth Rs. 30,000 – a loss of about 27% of potential returns.

Top 5 performing days (Jan 2014 – Sep 2024)

Impact of missing top 5, 10, 20, and 30 days

The current value of the Rs.10,000 invested in Nifty 50 during January 2014 is around Rs.41,000, as of September 2024 but if one has missed the top performing 5 days of Nifty50 shown above then the current value will be only around Rs.30,000 which is around ~27% fall in returns.

Similarly if one misses the top 10, 20 and 30 days, the fall in returns would have been -40%, -55% and -65% respectively.

This demonstrates the difficulty of predicting market movements, making staying invested a smarter option for long-term success.

What should investors keep in mind?

~add{num,1}

Stick with Systematic Investment Plans (SIPs)

SIPs allow investors like Mr. Sridhar to stay disciplined during market ups and downs. They benefit from cost averaging, meaning Mr. Sridhar buys more units when prices are low and fewer units when prices are high, which reduces risk over time.

This is called time diversification, spreading your investments across multiple periods to smooth out the price fluctuations.

~add{num,2}

Review your Financial Goals

Before making decisions during market highs, it’s essential to align your investments with your financial goals and risk tolerance.

~add{4,blog_highlight-block}

Example 1: Mr. Sridhar (Long-Term Goals)

At age 35, Mr. Sridhar doesn’t have any urgent financial goals, so he can afford to remain invested in equities even when the market is at its peak. His long-term goal allows him to withstand any short-term volatility.

Example 2: Mr. Kumar (Short-Term Goals)

Mr. Kumar, who has been investing for his daughter’s wedding next year, may want to liquidate part of his equity investments at the market peak. Since he needs the funds soon, he can transfer them to safer, fixed-income options like bonds or fixed deposits, which protect his capital from market volatility.

Conclusion

Markets naturally move in cycles. While it’s tempting to make impulsive decisions during a bull run or a correction, sticking to a well-thought-out plan and avoiding emotional decisions can help you stay on track to achieve your financial goals.

~add{3,blog_highlight-block}

Summary

To make your life easier, we have summarised the above Read here. Hope you enjoyed it!

Be the CEO of your Finances

Get practical and actionable money insights delivered straight to your inbox.